7 Tips for Breaking the Cycle of Poverty

By Lauren Bringle

Published on: 03/20/2019

Published on: 03/20/2019

If you look at the numbers, the inequality between the haves and have-nots is kind of devastating. Whether high poverty is inherited from generation to generation, caused by an emergency or something else, the need to take back control and better their financial situation keeps many people up at night.

Unfortunately, the stats about poverty skew heavily towards people of color too, and suggest a vicious cycle that can be difficult to break. Long-standing discriminatory practices among financial institutions have played their role as well.

Here are just a few eye-openers, according to a CFSI report.

No matter who you are, building wealth and overcoming poverty can be a challenge – but it is possible. Here are some tips for some small things you can do, starting now, to help break the cycle of poverty and take back control of your financial situation.

For starters, make sure you understand:

For basic financial literacy, try reading our blog, for one. Or check out sites such as NerdWallet or Credit Karma. Another option is to visit the Center for Financial Services Innovation (CFSI). CFSI is a leading authority on consumer financial health and in helping financial services deliver better consumer products and practices.

Make sure you know your rights, too. Visit the Consumer Financial Protection Bureau (CFPB). This company exists to make sure banks, lenders and other financial companies treat you fairly.

They have programs for financial coaching and adult financial education, etc, and other resources.

Basically, arm yourself with knowledge. Sometimes that’s your best defense.

To start changing your mindset towards money, take a moment to assess where you're coming from and where you stand right now with your finances.

Consider asking yourself these questions, for starters:

What’s the difference? When you think about your financial situation as a temporary status, you start to understand it’s something you can change. In other words, you have income mobility. If you make the right decisions and get smart with your finances, you can start to move up the “wealth chain” to a higher wealth situation.

Sometimes, just having the hope that things can change for the better – and that you can change your situation – can be pretty powerful. So take back your power when it comes to money.

Need financial advice or more active help? Having trouble understanding your taxes or how to start investing? Or have questions about other areas of finance where you could benefit from an expert’s help?

Don’t struggle alone in silence, take advantage of the resources available in your local community. Think of these resources as yet another way to improve your financial education. As great as reading online can be, sometimes it’s both nice and helpful to have face-to-face interaction.

Here are some places you can find free or lower-cost help:

If you have more income to devote to bettering your financial situation, you might also consider a certified financial educator, counselor, or advisor, who could help you get on the right track.

In fact, about 12 million Americans use payday loans each year, and spend an average of $520 in fees to borrow just $375. I don’t know about you, but that math just doesn’t add up.

As explained by the CFPB, the cost of a payday loan could range from about $10 to $30 for every $100 you borrow. Basically, if you take out a two week payday loan with a fee of $15 for every $100 borrowed, your Annual Percentage Rate (APR) would be nearly 400%.

To put this into perspective, the APR for credit cards runs from about 12-30%. But if you don’t have access to credit or credit cards, what are your options?

If you have a friend or family member who’s good with money, see if they’re comfortable letting you pick their brain and learn from their insights and mistakes.

Ask them what they did. Ask them what worked and what didn’t. Ask them what products they used and what financial products they like (or don’t like). Ask them how they budget and how they decide what to spend their money on. You might be surprised what tips people have you might not have considered before.

And if you don’t know someone personally, try to find someone online. Here are a few possible options you could consider:

The point is, you don’t have to go through this journey alone. There are so many people out there rooting for you, and so many people ready to help. You just have to take advantage of what they’re offering.

As Naseema of Financially Intentional says:

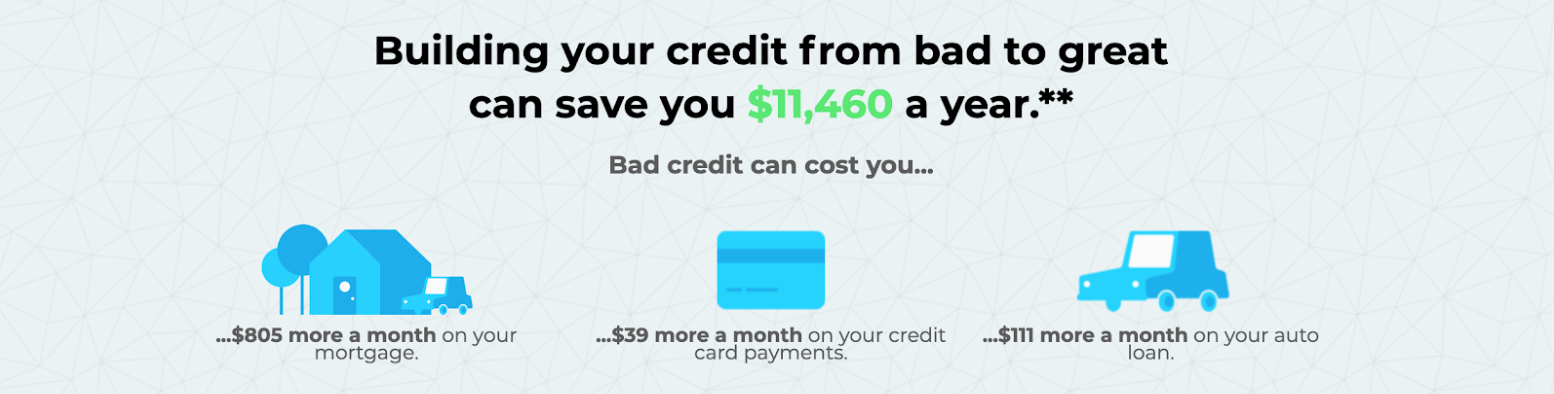

(**Assumptions: 30 year period with a $2,000 limit credit card every month; $250,000 mortgage with a 30 year term; a 48 month car loan.)

Basically, bad credit could cost you more in interest rates, car insurance costs, and limit your access to borrowing power.

Bad credit could cost you in ways other than just dollars and cents too. In many states, it can even impact the types of jobs you qualify for. In fact, 72% of employers now conduct background checks on employees before they’re hired, and 29% of those employers perform a credit check.

One of the best ways to break the cycle of poverty then is to build your credit responsibly. There are many ways you can get started with establishing or rebuilding your credit, depending on your individual situation.

First, make sure you understand how credit works, how your credit score is determined, and how you can build better credit for yourself. You can get started by reading the blog “The Simple Guide to Building Credit (and Saving Money)”.

Remember, building your credit isn’t a quick fix and it’s not a one-and-done thing – it’s the work of a lifetime. (See our article about how long it takes to build credit.) But if you take the right steps and manage your credit wisely, you can gain access to better financial products, better loans and more buying power over time. And hopefully even break the cycle of lower wealth.

You have options, so be sure to find a financial institution that will treat you right. After all, financial institutions profit from your relationship with them, so the least they can do is treat you with respect.

Remember that regardless of what anyone might tell you or try to make you believe, you have more options than you realize. So do your research and find what’s right for you.

Unfortunately, the stats about poverty skew heavily towards people of color too, and suggest a vicious cycle that can be difficult to break. Long-standing discriminatory practices among financial institutions have played their role as well.

Here are just a few eye-openers, according to a CFSI report.

- Only 23% of African Americans and 22% of Hispanics are financially healthy, compared to 50% of white individuals.

- At their current rates of income growth, it’ll take the average African American family 228 years to attain the same level of wealth as their white counterparts. It’ll take the average Latino family 84 years.

No matter who you are, building wealth and overcoming poverty can be a challenge – but it is possible. Here are some tips for some small things you can do, starting now, to help break the cycle of poverty and take back control of your financial situation.

1 - Educate Yourself

This one comes first because it’s the most important. The simple truth is the less you know, the more susceptible you are to getting taken advantage of - especially when most schools don't currently provide educational opportunities in financial literacy. So education is key.For starters, make sure you understand:

- Basic financial literacy

- How credit works and how to build credit responsibly

- Your options when it comes to financial products and institutions

- Your rights when it comes to banking and financial products

- If you’re shopping for credit cards, make sure you know the available Annual Percentage Rates (APR) – AKA how much interest you’ll be charged if you miss a payment.

- If you’re shopping for a loan, make sure you understand the amount of interest you’ll owe and other repayment terms, such as the length of the loan and your monthly payments. Lenders are obligated to provide you with the total cost of the loan and payment schedule.

For basic financial literacy, try reading our blog, for one. Or check out sites such as NerdWallet or Credit Karma. Another option is to visit the Center for Financial Services Innovation (CFSI). CFSI is a leading authority on consumer financial health and in helping financial services deliver better consumer products and practices.

Make sure you know your rights, too. Visit the Consumer Financial Protection Bureau (CFPB). This company exists to make sure banks, lenders and other financial companies treat you fairly.

They have programs for financial coaching and adult financial education, etc, and other resources.

Basically, arm yourself with knowledge. Sometimes that’s your best defense.

2 - Change Your Mindset Towards Money

“When it comes to improving your personal finances and achieving financial wellness, it’s 20% skill and 80% behavior and mindset,” Bola Sokunbi from Clever Girl Finance says.For many low-income workers, the hardest part of breaking the cycle of poverty is changing their mindset towards money. Their parents’ money habits and lessons may be deeply ingrained, strongly influencing their own attitudes toward money.

To start changing your mindset towards money, take a moment to assess where you're coming from and where you stand right now with your finances.

Consider asking yourself these questions, for starters:

- How were you raised with money?

- What money habits did you inherit from your parents? How did they handle money?

- What triggers you to spend your money? A raise, for example? A sale?

- What are your current money beliefs?

- How much do you own outright? How much money do you owe?

- What small steps can you take now to start changing these beliefs for the better?

What’s the difference? When you think about your financial situation as a temporary status, you start to understand it’s something you can change. In other words, you have income mobility. If you make the right decisions and get smart with your finances, you can start to move up the “wealth chain” to a higher wealth situation.

Sometimes, just having the hope that things can change for the better – and that you can change your situation – can be pretty powerful. So take back your power when it comes to money.

3 - Leverage Community Resources

While changing your mindset is helpful, having a positive mindset can only take you so far. At a certain point, it comes down to opportunity. As comedian Trevor Noah says in his book Born a Crime:“People love to say, ‘Give a man a fish, and he’ll eat for a day. Teach a man to fish, and he’ll eat for a lifetime.’ What they don’t say is, ‘And it would be nice if you gave them a fishing rod.’”The next step to mindset change involves finding the tools and helping hands you need to be successful. That’s where the resources available in your local community can come into play.

Need financial advice or more active help? Having trouble understanding your taxes or how to start investing? Or have questions about other areas of finance where you could benefit from an expert’s help?

Don’t struggle alone in silence, take advantage of the resources available in your local community. Think of these resources as yet another way to improve your financial education. As great as reading online can be, sometimes it’s both nice and helpful to have face-to-face interaction.

Here are some places you can find free or lower-cost help:

- Nonprofit organizations, such as United Way

- Public libraries or schools

- Some churches and community centers

- For taxes specifically, the IRS Tax Assistance Center

If you have more income to devote to bettering your financial situation, you might also consider a certified financial educator, counselor, or advisor, who could help you get on the right track.

4 - Avoid Predatory Payday Lending

If you just look at the name, a payday loan sounds like a loan that’s just for one day, right? But the truth is, if you get caught in the cycle of payday lending, you could be paying for that loan for years to come.In fact, about 12 million Americans use payday loans each year, and spend an average of $520 in fees to borrow just $375. I don’t know about you, but that math just doesn’t add up.

As explained by the CFPB, the cost of a payday loan could range from about $10 to $30 for every $100 you borrow. Basically, if you take out a two week payday loan with a fee of $15 for every $100 borrowed, your Annual Percentage Rate (APR) would be nearly 400%.

To put this into perspective, the APR for credit cards runs from about 12-30%. But if you don’t have access to credit or credit cards, what are your options?

“Payday loans encourage a cycle of debt thanks to high rates of interest, as well as high repayment installments. In most cases, the client will be unable to repay the debt by the due date. What happens next? Another costly loan is secured to cover the difference,” Financial Counselor Regina Blackwell says.Why do so many people keep falling into this trap? A few possible reasons:

- Emergency need for cash

- Poor credit or no credit, which is needed to access higher quality and lower interest loans

- Lack of awareness about other options

5 - Ask Someone you Trust

Sometimes, talking about money with a friend or loved one can feel awkward. But if you’re trying to better your finances, asking questions from those you trust can be the best way to help elevate yourself too.If you have a friend or family member who’s good with money, see if they’re comfortable letting you pick their brain and learn from their insights and mistakes.

Ask them what they did. Ask them what worked and what didn’t. Ask them what products they used and what financial products they like (or don’t like). Ask them how they budget and how they decide what to spend their money on. You might be surprised what tips people have you might not have considered before.

And if you don’t know someone personally, try to find someone online. Here are a few possible options you could consider:

- Bola from Clever Girl Finance

- Naseema from Financially Intentional

- Tiffany - AKA The Budgetnista

- Lacey, the Military Money Expert

- Eric from Personal Profitability

- Sean from One Smart Dollar

- Robert from the College Investor

- Sharita M. Humphrey

The point is, you don’t have to go through this journey alone. There are so many people out there rooting for you, and so many people ready to help. You just have to take advantage of what they’re offering.

As Naseema of Financially Intentional says:

“The key is to surround yourself with people who you aspire to be or are on the same path. Expand your knowledge, read personal finance books, listen to podcasts, and become a member of an online community. Be OK with getting uncomfortable and doing things differently than what you are used to. Stop looking for 'get rich quick' schemes. It will take some time, so get started as soon as possible.”

6 - Focus on your Credit

“Credit scores and history play a critical role in an individual’s ability to achieve economic security and build wealth in the U.S., but that opportunity is not easily attainable for communities of color,” a report by CFSI says.Whoever you are, having bad credit could cost you big time over the course of your lifetime.

(**Assumptions: 30 year period with a $2,000 limit credit card every month; $250,000 mortgage with a 30 year term; a 48 month car loan.)

Basically, bad credit could cost you more in interest rates, car insurance costs, and limit your access to borrowing power.

Bad credit could cost you in ways other than just dollars and cents too. In many states, it can even impact the types of jobs you qualify for. In fact, 72% of employers now conduct background checks on employees before they’re hired, and 29% of those employers perform a credit check.

One of the best ways to break the cycle of poverty then is to build your credit responsibly. There are many ways you can get started with establishing or rebuilding your credit, depending on your individual situation.

First, make sure you understand how credit works, how your credit score is determined, and how you can build better credit for yourself. You can get started by reading the blog “The Simple Guide to Building Credit (and Saving Money)”.

Remember, building your credit isn’t a quick fix and it’s not a one-and-done thing – it’s the work of a lifetime. (See our article about how long it takes to build credit.) But if you take the right steps and manage your credit wisely, you can gain access to better financial products, better loans and more buying power over time. And hopefully even break the cycle of lower wealth.

7 - Don’t be Afraid to Walk Away

If you have a bad feeling about a financial product or institution, or something doesn’t sound right, don’t be afraid to walk away. If a bank or lender is trying to hide stuff, or not being honest and transparent, walk away. If you feel you’re being discriminated against, walk away.You have options, so be sure to find a financial institution that will treat you right. After all, financial institutions profit from your relationship with them, so the least they can do is treat you with respect.

“You work too hard for your money to be treated poorly, and at the end of the day, financial institutions profit from your savings, investments and even your debt. So you should be treated respectfully,” Bola from Clever Girl Finance says.This is another instance where asking the people you trust could come into play. Find out where they’ve had a good experience and go there. Ultimately, remember that your money is power. So put it in the places you want to support, and the places where they’ll support you back.

Remember that regardless of what anyone might tell you or try to make you believe, you have more options than you realize. So do your research and find what’s right for you.

About the author

Lauren Bringle is an Accredited Financial Counselor® with Self Financial – a financial technology company with a mission to help people build credit and savings. See Lauren on Linkedin and Twitter.Editorial Policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).Written on March 20, 2019

Self is a venture-backed startup that helps people build credit and savings.

Self does not provide financial advice. The content on this page provides general consumer information and is not intended for legal, financial, or regulatory guidance. The content presented does not reflect the view of the Issuing Banks. Although this information may include references to third-party resources or content, Self does not endorse or guarantee the accuracy of this third-party information. Any Self product links are advertisements for Self products. Please consider the date of publishing for Self’s original content and any affiliated content to best understand their contexts.