What Credit Score Do You Need to Lease a Car?

Published on: 06/05/2023

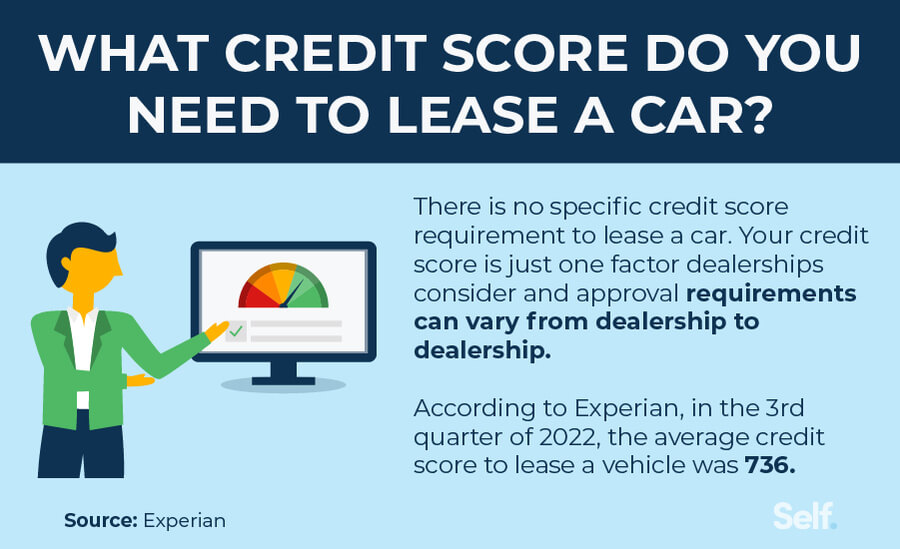

There’s no specific minimum credit score requirement to lease a car. Your credit score is just one factor dealerships consider when deciding to approve you for a lease, and approval requirements can vary from dealership to dealership. But typically, the higher your credit score is, the more likely you are to be approved and the better your leasing terms will be.[1]

According to Experian, in the 3rd quarter of 2022, the average credit score to lease a vehicle was 736.[2] If your score is below that, it doesn’t mean you can’t lease a car. However, the lender might see you as a higher risk for default and you might receive less favorable lease terms than if you had a higher credit score.[1]

This post helps you understand the ins and outs of leasing a car and how your credit score and credit history might impact your lease terms as well as your chance at approval.

Table of contents

- Credit score borrower risk profiles

- Can you lease a car with bad credit?

- Does leasing a car affect your credit score?

- Pros of leasing a car

- Cons of leasing a car

- Alternatives to leasing a car

- How to check your credit score for free

- How to improve your credit

Credit score borrower risk profiles

When lenders assess your credit, they evaluate how likely you are to pay as agreed. One factor they consider is your FICO® Score, and borrowers have scores that typically fall into categories referred to as borrower risk profiles.[3]

Although the scores fall into the five ranges in the table below, lenders typically refer to borrowers as prime, meaning you are least likely to default on your payments, and subprime, meaning you are more likely to default. So when leasing a car, where your score falls in these risk profiles may impact your lease’s monthly payment or your lease terms.[3]

| Borrower risk profile | FICO Credit score |

|---|---|

| Deep subprime | Below 580 |

| Subprime | 580–619 |

| Near-prime | 620–659 |

| Prime | 660–719 |

| Super-prime | 720 or above |

Keep in mind that you may have multiple credit scores depending on the credit scoring model used. One dealership may use a different model than another, resulting in a higher or lower credit score.

Can you lease a car with bad credit?

You may be able to lease a car with bad credit. However, the lender may see you as a higher risk for default, so you might receive less favorable lease terms to compensate for that risk.[1]

How each leasing company calculates your monthly payment might also vary slightly. They typically factor in:

- How much the vehicle will depreciate over the time period of your lease

- Taxes

- Additional fees, like a financing fee or a lease fee (similar to interest on a loan), which is known as a “money factor”[4]

If you have a low credit score, consider shopping around to compare lease offers. Different car makers all have different lease deals. You may think you have a bad credit score because it puts you into the subprime category, but, depending on the lease offer, you may be able to qualify for a lease that meets your needs by paying a larger down payment upfront or by adjusting other lease terms.

Does leasing a car affect your credit score?

Applying to lease a car is similar to applying for a car loan. The lender reviews several factors in addition to your credit score and credit report to assess the likelihood that you will pay what you owe as agreed. The lease application process could trigger a hard inquiry, which may temporarily lower your credit score.[5]

Because consumers tend to rate shop for certain types of loans, FICO® treats rate shopping for a lease differently. Although a hard inquiry appears on your credit report for each lease application, FICO® treats them as one inquiry as long as they fall between 14 days for older FICO® Score versions and 45 days for newer versions.[5]

Once you have an active car lease, you’re responsible for making your lease payments. If you miss a payment on a lease, it may negatively impact your credit score. On the other hand, if you make on-time payments on your lease each month, your account can help you build credit and could potentially lift your credit score. Payment history is the most significant factor in your credit score, making up 35% of your FICO®.[6]

Pros of leasing a car

Leasing a car can be a great option if you aren’t ready or able to purchase. Here are some of the benefits.

You may have lower monthly payments

The monthly payments on an auto lease are typically lower than the auto loan payments for the exact same vehicle. You’re only paying for the car’s depreciation during the lease period with mileage limitations, but also pay upfront fees and the money factor, which is equivalent to your interest rate.[7]

You avoid the hassle of selling your car

Leasing a car means you’re paying to use it for an agreed-upon amount of time and miles. At the end of the lease, you return the car to the dealership. You don’t have to worry about selling your car, but you will pay for wear and tear when you turn your car in if you didn’t take care of the car.[8]

You also don’t have to think about the car’s trade-in value — the amount of money a car dealer may pay for your old car towards the purchase of a new car — which can be difficult to calculate.[9]

Newer cars require less maintenance or repair

Compared to used vehicles, new leased cars may have fewer maintenance issues because you are driving a brand new car. While a used car may have a cheaper monthly payments, leased vehicles may cover more maintenance and repair issues within the manufacturer’s warranty.[8]

You may receive a bumper-to-bumper car warranty

Newer cars also typically come with a bumper-to-bumper warranty period. These warranty plans help cover the cost of repairs for the car if any are needed. With a used vehicle, you may have to pay extra for this type of warranty coverage.[10]

Cons of leasing a car

Leasing a car can be a great option, but it isn’t for everybody. Here are some of the potential downsides.

You will need to pay for any excess wear and tear charges

You may be required to pay for any wear and tear on the vehicle when you return it. If you damage the vehicle or don’t maintain it well over the course of your lease, you might end up paying additional costs to compensate.[8]

You are limited to a specific number of miles

Lease agreements specify the mileage you’re allowed on your leased vehicle. If you go over that limit, you usually have to pay an excess mileage penalty. You can add miles to your lease agreement before signing, but that typically results in a higher monthly payment. If you don’t use the miles, you don’t get that money back as a credit.[11]

You do not own the car

When you’re leasing a car, you’re borrowing it for a set amount of time and miles. At the end of the lease, you return the vehicle, so unless you plan to start another lease or have another car to drive, you have no vehicle.[8]

If you want to end your lease early, there may be a termination fee

If you decide you don’t like the car, or want to end your lease early for any reason, you may be charged a termination fee. Early termination fees are typically the difference between the balance remaining on the lease and the amount credited to the vehicle.

These fees can be pretty steep. Typically, the early termination charge is the difference between the balance you have remaining on your lease (lease payoff amount) and the amount credited for the vehicle (the vehicle’s realized value). For example, if your lease early termination payoff is $15,000, and you have $13,000 credit for the vehicle, then your early termination charge will be $2,000 ($15,000 minus $13,000).[12]

Alternatives to leasing a car

If leasing a car isn’t quite right or feasible for you, there are other options. Here are some alternatives to leasing a car to consider.

- Lease transfers: A lease transfer allows you to take over someone else’s car lease. That means, if you’re approved, you inherit their lease terms.[13]

- Car sharing: Although not available in all states, car sharing allows you to rent a car from a private owner for a short period of time through a rental company. The car owner is completely responsible for maintenance, and while many services may offer insurance, you should see if your personal insurance covers you as many policies don’t cover ride sharing.[14]

- Car rentals: Similar to car sharing, you can rent a car from a rental company. The rental company usually offers a standardized fleet of vehicles, and is responsible for maintaining the car in peak condition. Check your insurance policy to see if covers your rental car and how much; otherwise, you may have to pay the rental company for coverage or extra coverage[14]

- Buying a used car: Buying a used car from a person or used car dealer rather than a new car from a dealership typically comes at a lower cost. However, make sure the car is in good working condition before you purchase.[8]

How to check your credit score for free

By law you can check your credit report once a year for free from each of the major credit bureaus, which you can access at AnnualCreditReport.com. However, due to the COVID pandemic, the three major credit reporting bureaus (Experian, Equifax and TransUnion) will continue to offer free credit reports weekly through the end of 2023. Experian offers access to a free credit score when you set up a free account.[15]

How to improve your credit

Bad credit can be a major barrier to a lot of major financial decisions and opportunities. But, no matter where you’re starting from, there are ways to work toward good credit. Here are some strategies to try:

- Take out a credit builder loan. A credit builder loan works differently than a traditional loan. You don’t receive a lump sum after signing your agreement and then pay it back in installments. Instead, after approval, your loan funds are placed into a certificate of deposit (CD) or savings account, and you make your monthly payments. After your term is over and you’ve made all your payments, you get your lump sum (minus interest and fees). Your payments get reported to the credit bureaus as well so that you build both savings and credit.

- Sign up for a secured credit card. A secured credit card requires a cash security deposit be paid upfront, which is typically placed in a CD or savings account. You apply for the card, and once approved, you pay the cash security deposit, which acts as your credit limit, and then you can use the card to make charges up to the amount you deposited.

- Make on-time payments. Payment history is the most important factor in making up your credit score. Making on-time payments on all your credit accounts over time will have a positive impact on your score.[6]

- Review your credit report for any inaccuracies. Monitoring your credit is an essential part of staying on top of your finances. If you notice any inaccuracies, like debt that isn’t yours or suspicious activity, report it to the credit bureaus immediately so that it doesn’t harm your credit.

Working to improve your credit can be overwhelming, and it takes time and patience. However, Self has resources and information to support you every step of the way.

Disclaimer: FICO is a registered trademark of Fair Issac Corporation in the United States and other countries.

Sources

- Experian. “What Auto Loan Rate Can You Qualify for Based on Your Credit Score?” https://www.experian.com/blogs/ask-experian/auto-loan-rates-by-credit-score/. Accessed January 31, 2023.

- Experian. “State of the Automotive Finance Market Q3 2022,” https://www.experian.com/content/dam/noindex/na/us/automotive/finance-trends/2022/q3-2022-state-of-automotive-finance.pdf. Accessed January 31, 2023.

- myFICO. “Prime vs. Subprime Loans: How Are They Different?” https://www.myfico.com/credit-education/blog/prime-vs-subprime-loans. Accessed January 31, 2023.

- Investopedia. “Money Factor: Definition, Uses, Calculation and Conversion,” https://www.investopedia.com/terms/m/money-factor.asp. Accessed January 31, 2023.

- myFICO. “Credit Checks: What are credit inquiries and how do they affect your FICO® Score?” https://www.myfico.com/credit-education/credit-reports/credit-checks-and-inquiries. Accessed February 6, 2023.

- myFICO. “How Payment History Impacts Your Credit Score,” https://www.myfico.com/credit-education/credit-scores/payment-history. Accessed January 31, 2023.

- Federal Trade Commission. “Financing or Leasing a Car,” https://consumer.ftc.gov/articles/financing-or-leasing-car. Accessed January 31, 2023.

- Consumer Reports. “Leasing vs. Buying a New Car,” https://www.consumerreports.org/buying-a-car/leasing-vs-buying-a-new-car-a9135602164/. Accessed January 31, 2023.

- KBB. “Car Trade-in Tips: How Can I Maximize My Car’s Value?” https://www.kbb.com/car-advice/car-trade-in-tips-what-is-it-and-how-can-i-maximize-my-cars-value/. Accessed January 31, 2023.

- U.S. News & World Report. “Bumper-to-Bumper Warranty Guide,” https://cars.usnews.com/cars-trucks/advice/bumper-to-bumper-warranty. Accessed January 31, 2023.

- U.S.A. Today. “End your car lease without getting dinged,” https://www.usatoday.com/story/money/cars/2017/08/07/end-your-car-lease-without-getting-dinged/537553001/. Accessed January 31, 2023.

- Federal Reserve. “FRB: Vehicle Leasing: Up-Front, Ongoing, and End-of-Lease Costs,” https://www.federalreserve.gov/pubs/leasing/resource/consider/endclosed.htm. Accessed January 31, 2023.

- Federal Reserve. “FRB: Vehicle Leasing: Frequently Asked Questions,” https://www.federalreserve.gov/pubs/leasing/resource/faq.htm. Accessed January 31, 2023.

- Hertz. “Car rental vs. car sharing,” https://www.hertz.com/us/en/blog/resources/car-rental-vs-car-sharing. Accessed January 31, 2023.

- Consumer Financial Protection Bureau. “How do I get a copy of my credit reports?” https://www.consumerfinance.gov/ask-cfpb/how-do-i-get-a-copy-of-my-credit-reports-en-5/. Accessed January 31, 2023.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.

Editorial policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).